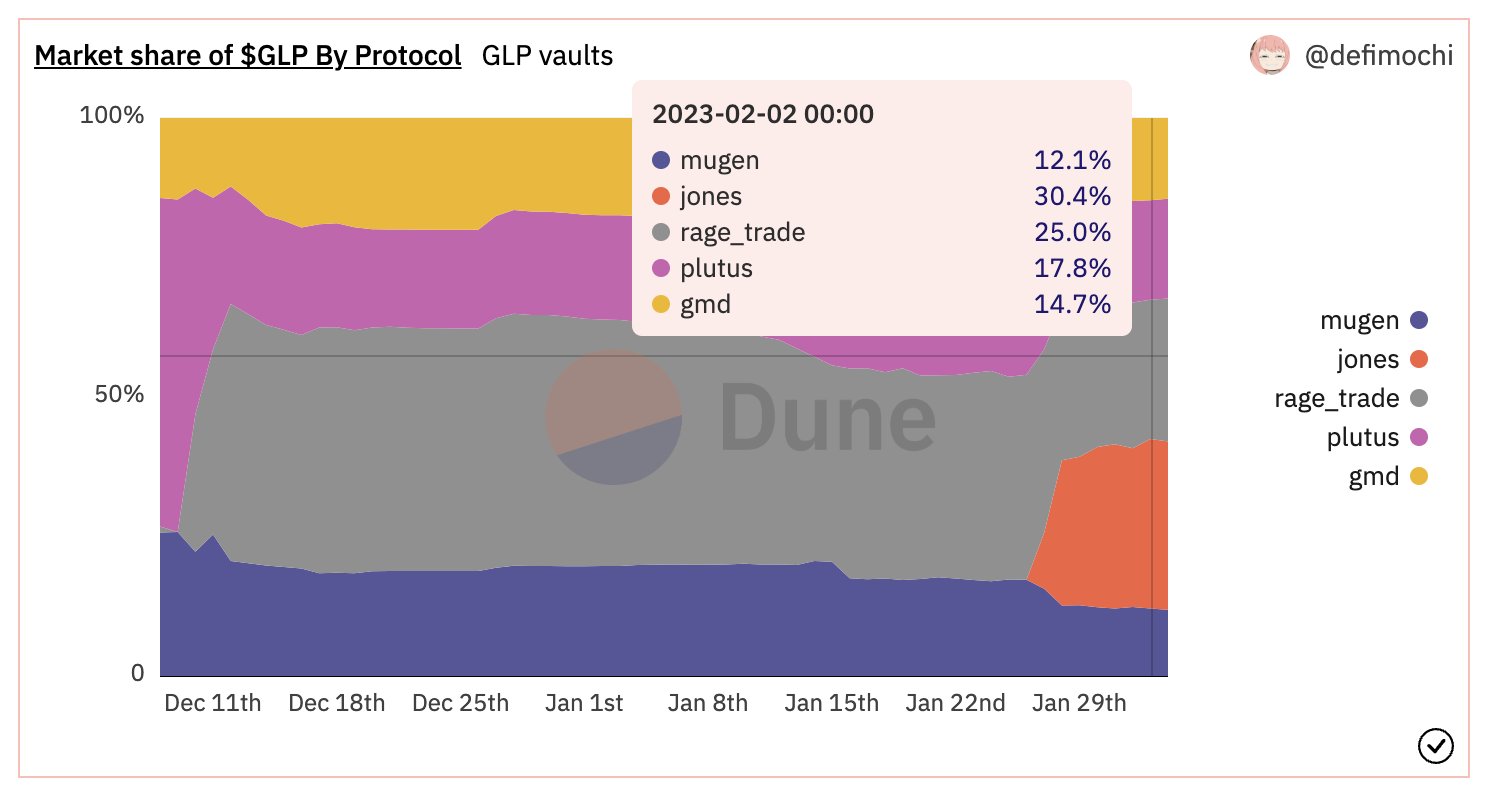

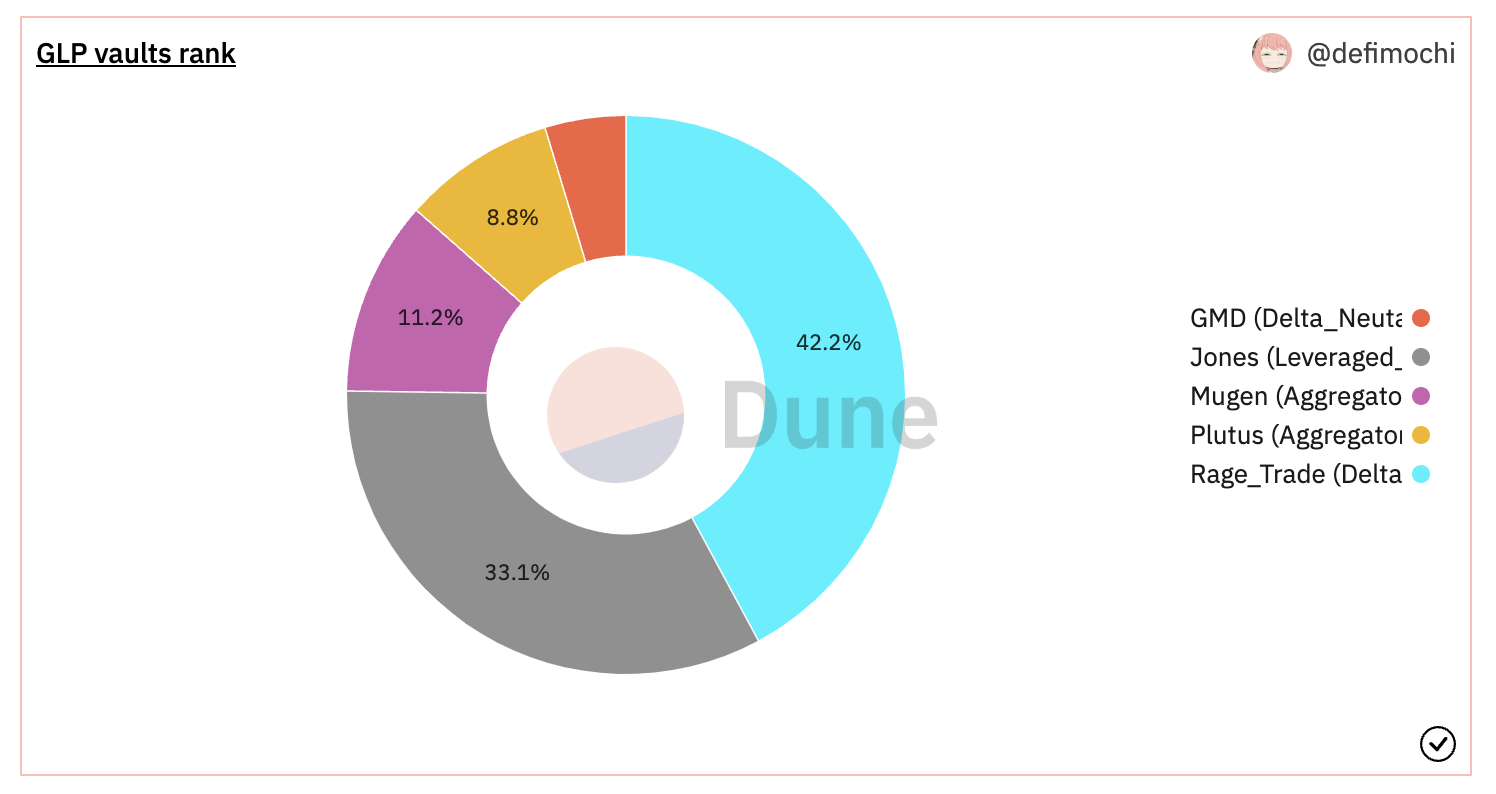

Occupy 28% Of GLP Market Share, Where Do Jonesdao's High Returns Come From?

According to the data chart released by @defimochi, jGLP has occupied more than 28% of the GLP market share in just one week, making rivals such as Mugen and Plutus all give up. What exactly is jGLP? Why can he quickly absorb a large amount of GLP? This Coincu article will explain the principles of jGLP and jUSDC pool one by one so that readers can understand the meaning of their high-yield sources.

JonesDAO is a DeFi revenue strategy protocol built on the Ethereum mainnet and Arbitrum.

It is mainly to build various types of fund pools, and each fund pool implements different strategies for user groups with different risk preferences. Currently, it provides three types of fund pools:

GMX is a decentralized exchange on Arbitrum. Its featured leveraged products allow users to have a centralized trading perpetual contract-like experience. Market makers who want to become GMX need to deposit and mint GLP tokens. GLP itself is GMX’s mixed multi-asset fund pool, which provides liquidity for other trading users, and the GLP token is the equity share token of the pool.

There is a basket of assets in the GLP pool, half of which is stablecoin and half is not a stablecoin. These assets become the counterparty of all traders. GLP token holders can charge 70% of the transaction fee (issued weekly, ETH).

Note that although GLP is a token in ERC-20 standard, it cannot be traded or transferred in any place other than GMX because there is no conventional transfer contract (GLP contract on Arbiscan) in its contract. Nevertheless, Staked GLP can be transferred and traded like other regular ERC-20 tokens.

From the perspective of the distribution of the GLP pool, 50% of the stable currency constitutes half of the funds in the GMX market, allowing these non-stable coins to be shorted, and it also makes the “position” of LPs (GLP holders) safer, but it may It discourages LPs, because for LPs, these stablecoins are opportunity costs, and they could have easily found higher returns with these assets in a bull market.

Quantumzebra wrote an excellent analysis of what happens to GMX in a bull market, and as he states, half the pool of stablecoins is useless if no one is shorting them. Traders will only lend BTC and ETH from the GLP pool for long bets.

In order to retain LPs, Jones DAO created the jGLP + jUSDC fund pool. They used a creative “off-market” allocation mechanism to increase the incentives of GLP holders after adding leverage and, at the same time, provide low-risk income products to USDC holders.

The jGLP pool mints more GLP by borrowing USDC from the jUSDC pool (so that it is leveraged and earns more ETH fees), and takes most of the new income, thereby increasing the income of GLP.

Users deposit GLP or any token in the GLP basket (UNI, LINK, ETH, WBTC) into the jGLP vault. (All baskets of tokens are first mortgaged into GLP in GMX by the smart contract of jGLP vault).

Users can withdraw GLP or any GLP component token (UNI, ETH, LINK, etc.) from the jGLP pool at any time, and the treasury will help users redeem it from GMX, but users need to pay the corresponding fees.

How many dollars will jGLP borrow to leverage? How much leverage is there? Will the leverage ratio change?

At present, we cannot find relevant data to show the exact leverage ratio, but JonesDAO stated that its capital pool adopts a dynamic leverage ratio, which is opposite to the market trend. When the market goes down, it goes up, and vice versa.

According to its official document, it only states that it borrows USDC within specific risk parameters and anchors the target leverage range.

The jUSDC pool is the source of liquidity for jGLP leverage. Suitable for users with low-risk appetites. The stablecoin lending income of this pool is higher than that of ordinary reception protocols such as AAVE and Compound.

Note that you need to initiate an application in advance to withdraw coins from the jUSDC pool, and the withdrawal can be opened after 24 hours.

jGLP holders mainly benefit from three aspects:

Additional sources of incentives: automatic compounding rewards and withdrawal penalties

Withdrawals from jGLP are subject to a 3% fee on the total position. 1/3 of this will be distributed to other depositors as a no-withdrawal bonus. 2/3 will be distributed to users (holders of jGLP receipt tokens) who have opted for automatic compounding.

Users of jUSDC will mainly benefit from the rate of return on the leveraged part. Withdraw from jUSDC, you also need to pay other jUSDC users 0.97% of their position size as a retained “non-withdrawal reward.”

However, the actual rewards received by the remaining jUSDC stakers are different from 0.97%. Real is the difference between the above amount (0.97%) and the actual cost of GMX redeeming USDC. When the cost is higher than the 0.97% fee, there will be no retention rewards.

Please note that when withdrawing USDC from the jUSDC fund pool, the first source of liquidity is the unused idle USDC in the pool. Withdrawals in excess will require the burning of the GLP implementation in GMX.

Please note that jGLP + jUSDC does not eliminate any opportunity cost or counterparty risk of GLP; on the contrary, it just increases the rate of return of directly holding GLP by means of leverage, making it more attractive, and This is achieved by borrowing money from other risk-averse users.

This pattern serves two types of users:

But for the latter (coin depositors of jUSDC), they actually bear the liquidity risk of GLP indirectly because their own money was also used for mint GLP, but they did not get the 100% return due to the risk (most of it was forked by jGLP) but only a part.

If there is a real USDC redemption run on GMX, jUSDC pool users will be greatly affected. As for whether the additional risk premium can cover these new risks, we still lack data support. Leverage ratio data and detailed fee structure are lacking in official documents and white papers. Therefore, DYOR should be cautious when making any decisions, and we will continue to follow up.

DISCLAIMER: The Information on this website is provided as general market commentary and does not constitute investment advice. We encourage you to do your own research before investing.

Join us to keep track of news: https://linktr.ee/coincu

Harold

Coincu News

BlockDAG crosses $170.5M in presale success with BDAG250 bonus and Whitepaper V3 launch! Solana grows…

Discover why Qubetics, Toncoin, and XRP are the best coins to invest in right now.…

Over the years, meme coins have evolved from inside jokes into serious investment opportunities.

Discover BlockDAG's five-tier bonus program's closing phases that enhance buyer holdings. Gain insights on the…

Discover why Qubetics, Solana, and Cardano are redefining the crypto landscape. Learn about milestones, price…

Discover why Qubetics, NEAR Protocol, and Immutable X are the best altcoins to join today,…

This website uses cookies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}