Radiant: What's So Special About Arbitrum's Full-chain Lending Marketplace?

Key Points:

They are comparable in terms of the money market. The primary distinction is that Radiant will be a full-chain currency market. Radiant users can undertake cross-chain lending on any of the chains that Radiant supports.

Users can deposit ETH, GMX, or MAGIC on Arbitrum (if there is liquidity), then borrow BNB on BSC, SOL on Solana, OP on Optimism, and Ethereum ETH, for example. Users of this loan method are not required to do asset cross-chain transactions (for example, they do not need to deposit their ETH on Arbitrum into Optimism). That is, borrowing and lending transactions can be accomplished on separate chains or L2 without cross-chaining assets to other chains from the user’s perspective.

At the moment, most lending protocols launch distinct versions on different chains/L2, such as Ethereum L1, Arbitrum, Optimist, BSC, Solanan, Avalanche, and so on. They are not interoperable with one another, and their liquidity is dispersed. Assets must initially cross-chain in order to function.

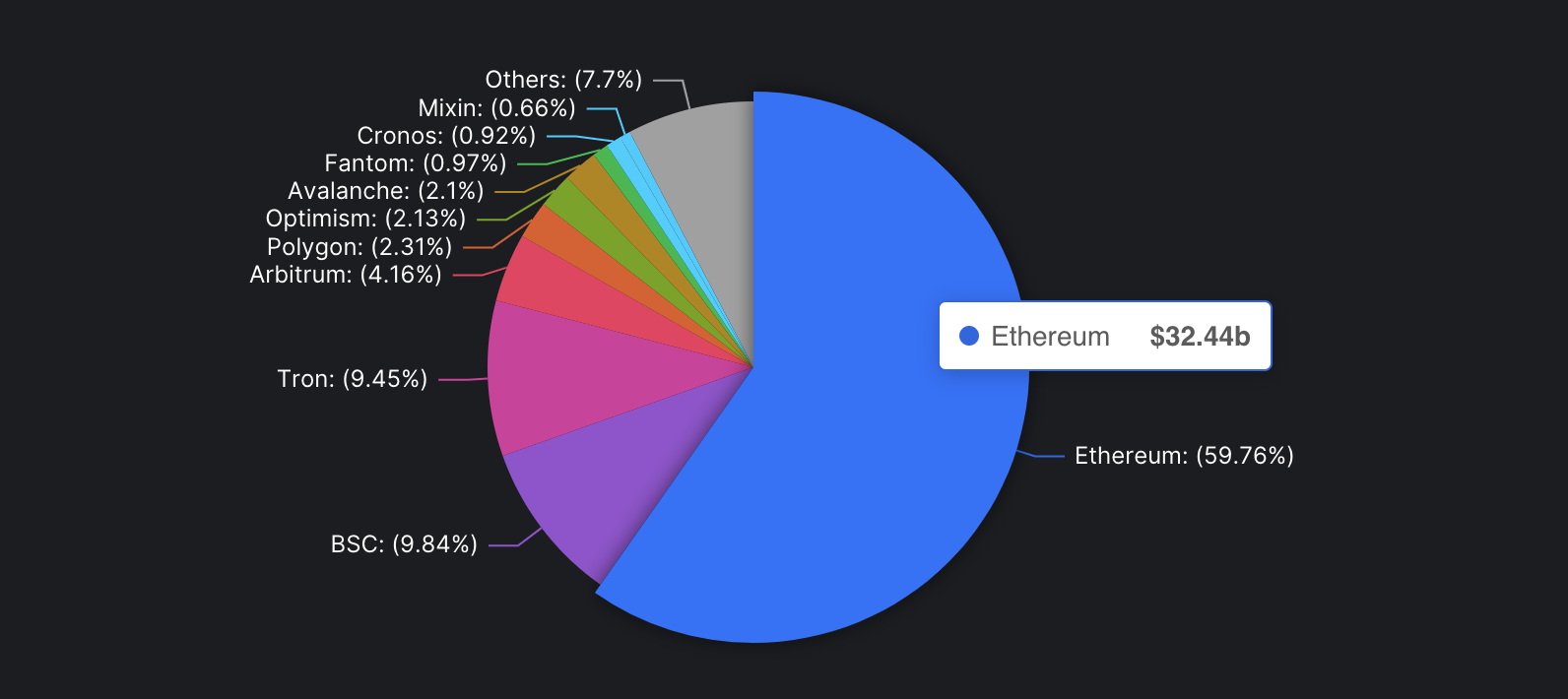

The purpose of the full-chain currency market is to integrate liquidity across several chains, decrease operational difficulties for regular users, and increase asset utilization. According to Defillama’s research, the TVL of Ethereum L1 is around 60% as of the authoring of Blue Fox Notes, with the remainder dispersed on several other chains. These chains’ loans and loans are carried out independently, and the liquidity is segregated.

To put it simply, Radiant employs LayerZero’s Omnichain technology to construct its full-chain interoperability.

Radiant attempts to overcome the problem of liquidity fragmentation between multiple chains/L2 by constructing a full-chain lending market.

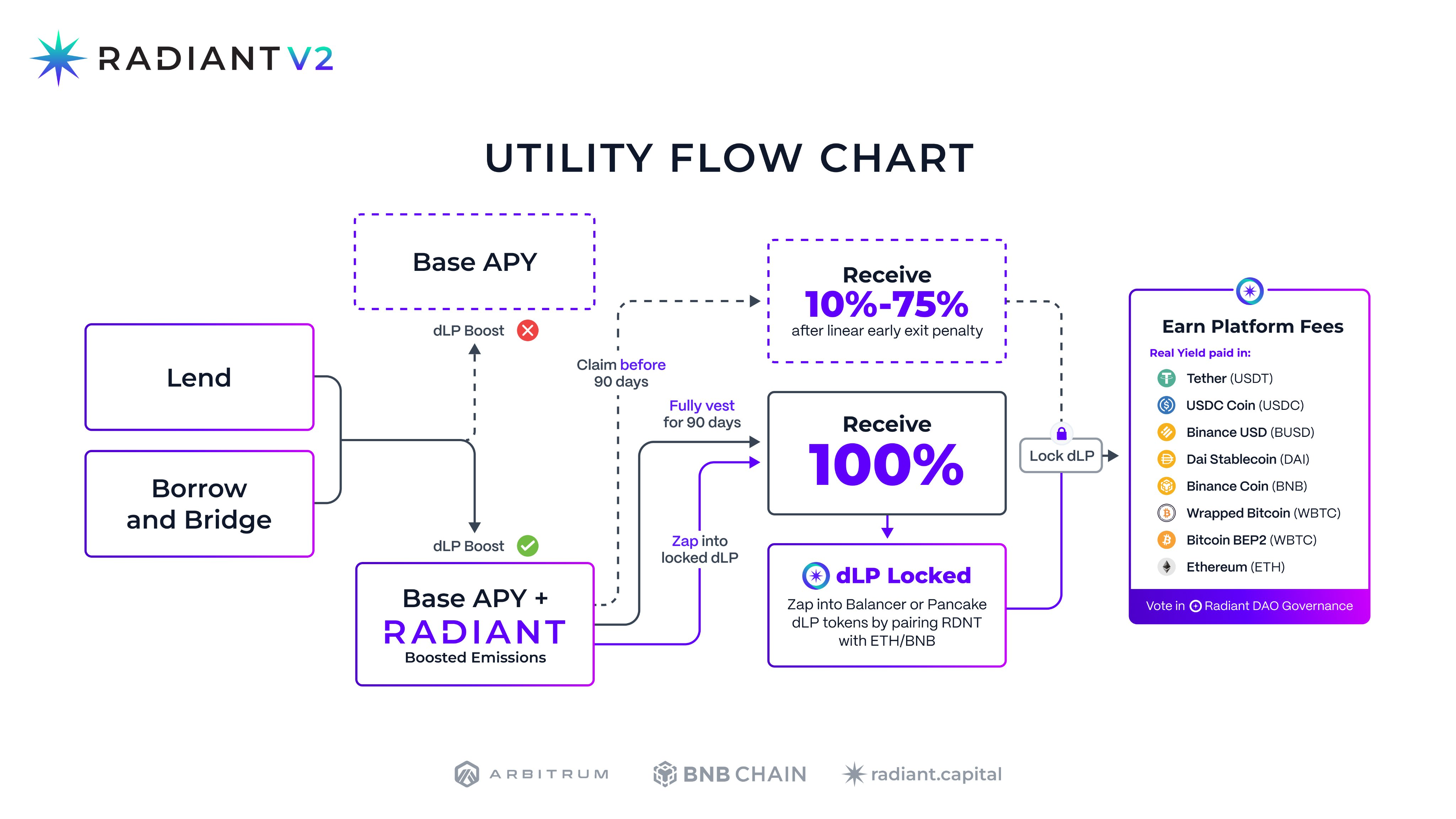

Radiant is now planning to introduce RDNT V2 in the next weeks, which will also be of interest to the community. In summary, the key points are as follows:

Radiant incentivizes borrowers and lenders with newly minted RDNT. The notion of dLP (dynamic Liquidity Provisioning), or dynamic liquidity provision, is introduced in RDNT V2.

Users must contribute a particular level of liquidity, and the value given by this liquidity must be at least 5% of their overall deposit value in order to receive incentives for more RDNT issuance. Because the value varies dynamically, it is referred to as dynamic liquidity provision.

If the specified liquidity value ratio is less than 5%, no extra RDNT issuance incentive will be collected. Depositors must contribute a specified amount of liquidity in this manner in order to get RDNT advantages. On the one hand, it can lock a certain proportion of RDNT and boost its demand; on the other hand, it can improve RDNT liquidity, therefore realizing the contributors’ symbiotic relationship and the agreement’s long-term development goals.

Its goal is to provide a seamless cross-chain experience that will encourage the incorporation of additional new chains.

In V1, customers must wait 28 days before withdrawing RDNT. If any time is advanced during this period, it will be decreased by 50%, which means that the last second of withdrawal from the 28th day will also be reduced by 50% of RDNT.

The vesting time is raised from 28 to 90 days in the V2 design, although early exit is lowered linearly. On the one hand, the vesting term is lengthened to lessen possible selling pressure; on the other hand, penalty reductions become more realistic as a result of the linear model.

Only locked RDNT can receive protocol fees in V2; no incentives will be granted after expiration.

In V1, the borrower’s fee will be split 50/50 between the RDNT locker and the lender, however in V2, 60% of the cost will go to the RDNT locker, 25% to the lender, and 15% to the RDNT locker. The DAO has been assigned %.

In other words, the RDNT stakeholders stand to benefit the most from future protocol fees. If the agreement is expanded, the more fees earned, the more RDNT pledge lockers will earn, causing more users to pledge RDNT, establishing a flywheel effect, and supporting loan market expansion. Yet, the opposite is also true; the death spiral is the flip side of the flywheel effect. Also, DAO receives 15% of the charge, which is used for future DAO development requirements.

Overall lending market size

At the time of writing, Radiant currently has an overall lending market size of around $408 million.

Protocol Fees for RDNT Participants

At the moment, the total price paid by RDNT pledgers is $5.91 million, which means that 50% of the fees created by the agreement are transferred to RDNT pledge vaults.

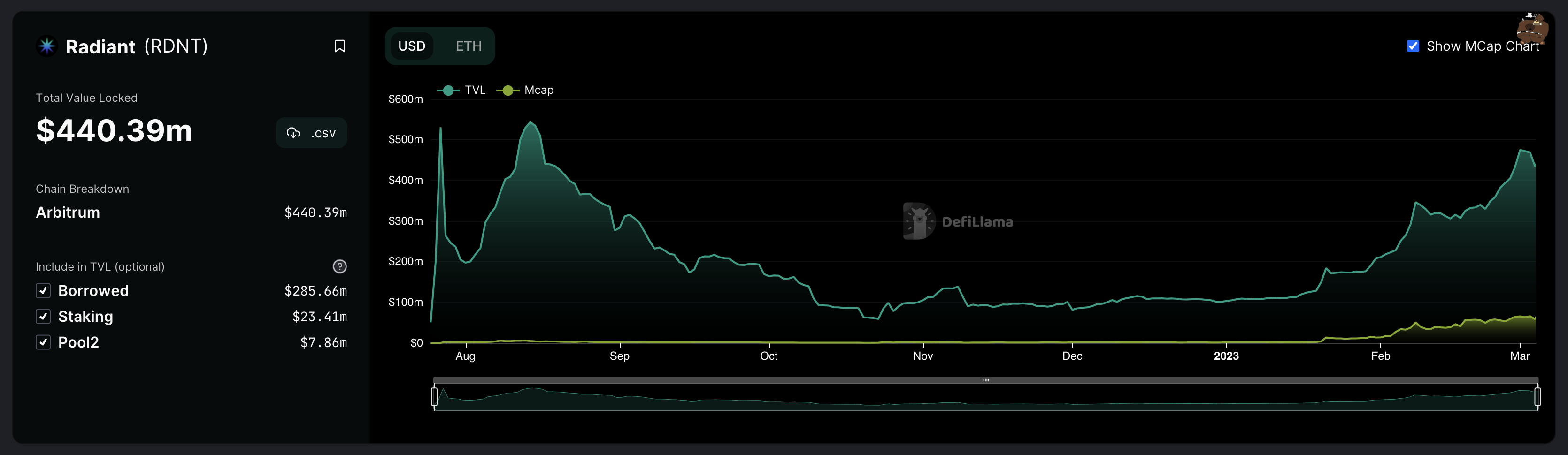

Total Value Locked

According to Defillama data, the current TVL of assets deposited in Radiant is $123 million; if borrowed, pledged, and Pool2 are added, the overall TVL is about 440 million.

According to the data shown above, Radiant is already a market leader in the Arbitrum loan sector. If the full-chain lending market can be expanded in the future, the market size may grow even more.

Lastly, there are possible threats in the DeFi field at all times, and this must be acknowledged. Radiant is both a technology and a protocol based on the LayerZero protocol. If there is an issue with LayerZero, Radiant will be affected as well.

In fact, LayerZero not only requires that the two roles of Relayer and Oracle will not conspire to do evil but also requires users to trust the developers who use LayerZero to build applications as a reliable third party and the trusted subjects participating in the “multi- signature” are all Pre-arranged privileged role.

At the same time, it did not generate any fraud proofs or validity proofs during the entire cross-chain process, let alone put these proofs on the chain and perform on-chain verification. Therefore, LayerZero does not Decentralized and Trustless at all.

In truth, LayerZero needs customers to trust the developers who utilize LayerZero to construct apps as a dependable third party, and the trusted subjects participating in the “multi-signature” are all Pre-arranged privileged roles.

At the same time, it did not create any fraud or validity evidence during the full cross-chain transaction, much alone place them on the chain and doing on-chain verification. As a result, LayerZero is neither decentralized nor trustless. Coincu also had an article on this topic.

DISCLAIMER: The Information on this website is provided as general market commentary and does not constitute investment advice. We encourage you to do your own research before investing.

Join us to keep track of news: https://linktr.ee/coincu

Harold

Coincu News

Read how Plus Wallet surpasses Rabby Wallet in providing users with enhanced freedom, rewards, &…

George Town, Cayman Islands, 18th December 2024, Chainwire

Explore the top coins to invest in for short-term gains in 2025. Qubetics, Polygon, and…

The Hong Kong SFC has licensed four additional cryptocurrency trading platforms, bringing the total to…

Singapore, Singapore, 18th December 2024, Chainwire

Binance Alpha, a new platform integrated into Binance Wallet, offers early access to promising cryptocurrency…

This website uses cookies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}