GMX Review: Powerful Perpetual Trading Platform On Arbitrum

Since its debut on Arbitrum in September, GMX has taken DeFi by storm. There are several reasons why this has piqued the interest of so many, ranging from top-tier developers constantly creating to sustained actual dividends for token holders during a down market.

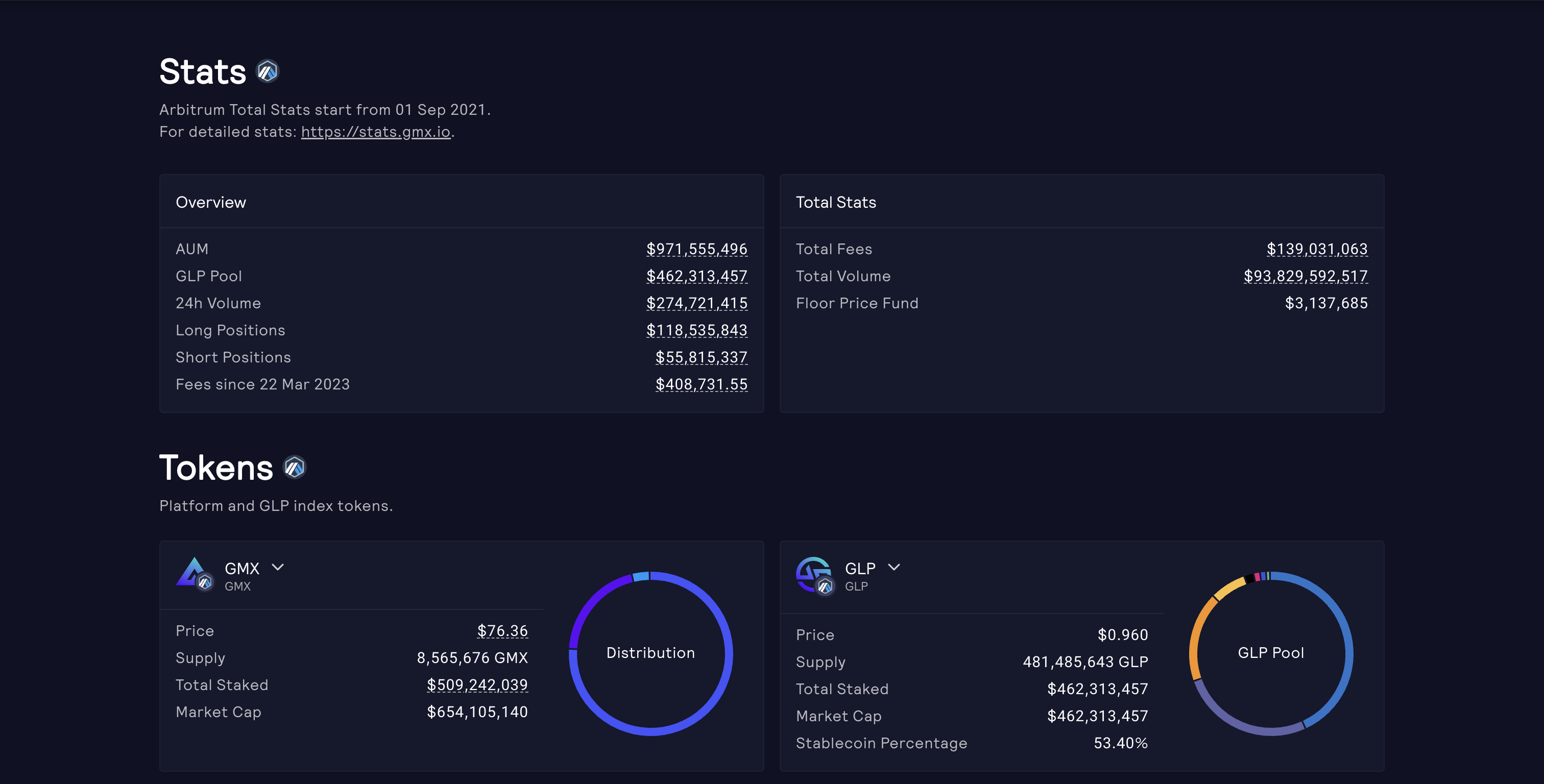

Because of its Rewards Program, the platform gained substantial interest in 2022. Users may earn up to 20% APY in protocol rewards from trading profits by purchasing and staking the GLP token, which is a basket of all tradable tokens on GMX.

The Arbitrum Layer 2 and Avalanche C Chain networks host GMX, a decentralized spot, and perpetual exchange. It was established by unknown developers headquartered in Sydney, Australia. With almost $94 billion in total trading volume and more than $160 million in daily open interest, the trading platform is the biggest in DeFi.

The platform mainly provides margin trading to anybody who does not meet the KYC or Professional Investor standards found on a CEX.

Margin trading is the process of borrowing funds to trade with, with collateral serving as the loan. The borrowed cash is then utilized to go long or short on an asset, with leverage defined as the connection between position size and collateral size. This results in a greater profit or loss than would be obtained by acquiring a spot item.

GMX is a well-known decentralized exchange that specializes in trading perpetual futures. The initiative, which was launched in late 2021 on the Ethereum Layer 2 network Arbitrum and then deployed to Avalanche, soon gained attention by allowing customers leverage of up to 30 times their deposited collateral.

In recent years, leverage trading has become a crucial component of the crypto ecosystem. It enables market players to benefit from price declines, limit risk in uncertain times, and gamble large on an asset when they have confidence.

There are various methods to get leverage in cryptocurrency. Customers may borrow money from Binance, FTX, and other centralized exchanges for trading purposes. Binance and FTX allow consumers to borrow up to 20 times their original payment. DeFi systems such as Aave and MakerDAO provide permissionless loans against crypto collateral.

GMX, on the other hand, is a decentralized exchange that provides leverage trading services. In that regard, it provides a comparable experience to other DeFi exchanges, such as Uniswap, while also providing leverage trading capabilities similar to Binance.

Users on the platform may get up to 30x leverage on BTC, ETH, AVAX, UNI, and LINK transactions. In other words, if a trader deposits $1,000 in collateral with GMX, he or she will be able to borrow up to $30,000 from the liquidity pool. Now, the GMX Review article will learn about the networks the project interacts with.

Arbitrum and Avalanche, two low-fee chains, are presently hosting GMX. Arbitrum is Ethereum’s leading Layer 2 and an Optimistic Rollup. Avalanche, on the other hand, has its own EVM Layer 1 chain with a distinct 3-chain design, and it is now the second biggest L1 after BSC.

The GMX Arbitrum platform outperforms the Avalanche version by providing more trading pairings, bigger payouts, and lower costs. Another reason consumers favor Arbitrum over Avalanche is that rewards are distributed in Ethereum (ETH) rather than Avalanche (AVAX), which has historically underperformed.

Traders may only trade assets that exist in the basket on each chain due to the unique multi-asset pool architecture of GLP (GMX’s liquidity pool).

GMX may assist traders in trading at a reasonable cost and with no arbitrage risk. It will employ its own liquidity pools to do this, and trading prices will be determined by Chainlink’s Oracle utilizing TWAPs (Time-Weighted Average Prices) from major DEXs.

The platform operates on the Arbitrum and Avalanche blockchains, both of which have low transaction fees and fast transaction speeds, resulting in a seamless transaction experience that saves time and money.

Due to the usage of its own liquidity pool model, it can support huge liquidity without having as many TVLs as the AMM model.

To offer liquidity on the platform, you may utilize a variety of tokens (ETH, BTC, LINK, UNI, USDC,…); while providing liquidity, you will earn GLP tokens; when not providing liquidity, you simply sell GLP to recover the tokens in the pool.

When you offer liquidity to hold GLP, you will have the opportunity to get 70% of all fees on the platform (in the form of ETH or AVAX) as well as extra Incentives from GMX (in the form of esGMX).

Moreover, holders of GMX tokens get 30% of the project’s earnings.

Unlike dYdX’s Orderbook approach, Perpetual Protocol’s AMM Pool, or CEX exchanges’ typical Spot Futures balancing methodology, GMX employs its own liquidity pools, and prices will be traded on Oracle.

Oracle prices are based on the average price of the main CEX and DEX exchanges.

When trading the Spot ETH – DAI pair on the GMX platform, for example, you will:

The same is true for the Margin and Perpetual features. When you long the ETH – DAI x20 combination, GMX will understand that you are borrowing x20 DAI to purchase ETH and doing Spot-style transactions with the quantity x20. While trading Long / Short on GMX, you will be charged fees such as:

GMX requires huge liquidity pools in order for the private Liquidity Pool concept to operate and for you to trade in high quantities.

As an incentive token for liquidity providers, the platform issued GLP. It is the GMX token that represents all pools. In other words, it is an index that reflects all assets utilized on GMX to offer liquidity.

That is, when you provide liquidity on the platform, you are offering liquidity to the whole asset on the exchange in a certain ratio, not just one token. As a result, when the value of all assets rises, so will the value of the GLP token, and vice versa.

The asset ratio will not be preset and selected by GMX to guarantee that the pool structure is not lopsided.

For example, the platform calculates the ideal ETH/USDC ratio to be 28% and 38%, respectively.

Yet, the current ETH rate is 27.65% (lower than optimum), whereas the USDC rate is 44.31%. (higher than optimal).

As a result, in order to decrease the rate of USDC in the Pool, GMX will cut the transaction cost when you purchase USDC in the Pool with other tokens. When selling USDC to other currencies, however, you may be charged extra costs.

GMX transaction fees now vary from 0.2% to 0.4%.

1.9% of the team’s GMX will be dispersed equally over the course of two years. The remainder is mostly paid via esGMX and MP, and this token will not have a defined payment schedule.

Users who have GMX tokens have the ability to vote on the project’s governance actions and development direction.

Fees on GMX have remained consistent for most of the year, with lulls in certain months, but Arbitrum, at the very least, is returning $1-3M in fees every week. Fees are especially high during periods of volatility because liquidations occur, traders make errors on significant market swings, and then continue to revenge trade to recoup their losses. Such instances are Luna, FTX, and Silicon Valley Bank, all of which occur when news causes the market to rise or fall substantially.

Trading commissions for opening and closing positions are 0.1%. Every hour, a variable borrow cost is deducted from the deposit. The swap cost is 0.33%. Since the protocol acts as the counterparty, there is little price effect when entering and departing deals. GMX says that depending on the degree of liquidity in its trading pool, it can execute huge deals precisely at mark price.

When a user decides to go long, they may give collateral in the token on which they are wagering. Any earnings they make are reinvested in the same asset. For shorts, collateral is restricted to the stablecoins supported by GMX: USDC, USDT, DAI, or FRAX. Gains on short positions are rewarded in the stablecoin that was utilized.

Updated to March 2023:

The 1.5% minimum profit rule has been removed. GMX used to require that the marked price must have moved by at least 1.5% for a position to be in profit. This has now been updated to a two-part transaction process without the 1.5% rule.

Finally, GMX has emerged as a key participant in the DeFi field, providing a decentralized trading protocol with margin trading features and an easy-to-use user interface.

It is one of the most unique and intriguing Decentralized Finance products. They provide a quick, seamless, and thoroughly liquid on-chain trading experience on Ethereum’s leading Layer 2 Arbitrum and Avalanche.

Considering the ongoing growth of the Arbitrum ecosystem, the potential of this initiative remains enormous. Hopefully the GMX Review article has helped you understand more about the project.

DISCLAIMER: The Information on this website is provided as general market commentary and does not constitute investment advice. We encourage you to do your own research before investing.

Join us to keep track of news: https://linktr.ee/coincu

Harold

Coincu News

Discover why Qubetics, Solana, and Cardano are redefining the crypto landscape. Learn about milestones, price…

Discover why Qubetics, NEAR Protocol, and Immutable X are the best altcoins to join today,…

BTFD Coin is offering a chance to relive the glory days of meme coin investing,…

Explore key takeaways from BlockDAG’s AMA, showcasing strides in scalability, growth of the ecosystem, and…

Discover why Qubetics, Polkadot, and Cosmos are the best cryptos with 1000X potential, offering innovation,…

Explore the best coins to buy in December 2024—Qubetics with its thrilling presale, Polkadot’s interoperability,…

This website uses cookies.

{kind=link}

{kind=link}

{kind=link}