Top 5 Uncollateralized Lending Projects In 2023

Crypto lending has emerged as a popular financial service, offering the opportunity to earn regular interest payments by lending deposited cryptocurrencies. This lending activity is typically facilitated on various platforms and has two primary categories: collateralized and uncollateralized lending.

In the world of cryptocurrency lending, collateralized loans have been the conventional choice. Borrowers secure these loans by offering collateral, which usually consists of other assets. By providing collateral, borrowers gain access to funds. This mechanism not only minimizes the risk for lenders but also allows borrowers to tap into additional liquidity.

Both decentralized and centralized crypto lending platforms offer lucrative interest rates, occasionally reaching up to 20% in annual percentage yield (APY). In these lending ecosystems, borrowers are generally required to deposit collateral, further reducing the risk for lenders. The decentralized platforms operate on blockchain technology, ensuring security and transparency, while the centralized platforms offer a more user-friendly experience.

Uncollateralized crypto lending, on the other hand, is a riskier endeavor for lenders. This lending model does not require borrowers to provide collateral, which can lead to increased risk. However, it provides borrowers with an opportunity to access capital without the need for collateral, offering more flexibility.

Uncollateralized crypto loans have primarily been the domain of businesses and institutions. These entities have leveraged these loans to free up capital that would otherwise be locked in collateral. This has allowed them to pursue a wider array of investment opportunities and trading strategies.

Within the world of uncollateralized crypto projects, there exists a unique category known as “flash loans.” These types of loans may be accessible to ordinary investors, offering a fascinating way to experiment with uncollateralized borrowing in the crypto market.

Uncollateralized crypto lending can be an attractive prospect for borrowers looking to access liquidity without tying up valuable assets as collateral. However, it’s important to note that this lending model is not without its risks. Lenders are exposed to the possibility of non-repayment, making uncollateralized lending inherently riskier compared to its collateralized counterpart.

TrueFi, which operates on the Ethereum blockchain and Optimism, is forging a path in the DeFi landscape by connecting investors, borrowers, and capital managers in uncollateralized lending, encompassing both crypto-native and traditional financial avenues.

The heart of TrueFi’s innovation lies in its commitment to disintermediation. By establishing asset management on-chain, TrueFi effectively eradicates the need for intermediaries, opening the door to a host of financial opportunities that were once the exclusive domain of the ultra-wealthy. This remarkable development has far-reaching implications for the DeFi sector and the broader financial ecosystem.

The TrueFi platform empowers lenders by offering superior yields on their loaned capital, challenging the traditional financial system where banks and other intermediaries have historically reaped the lion’s share of the profits. Investors can now directly engage in uncollateralized lending, participating in both cryptocurrency markets and traditional financial instruments. This approach offers them a more competitive edge, providing a previously unattainable level of financial access.

TrueFi’s groundbreaking platform has rapidly garnered attention and support from those looking to diversify their portfolios or achieve higher yields on their investments. Its disruptive approach to credit in DeFi marks a pivotal moment, as it challenges traditional financial models and brings unparalleled financial opportunities to a wider audience.

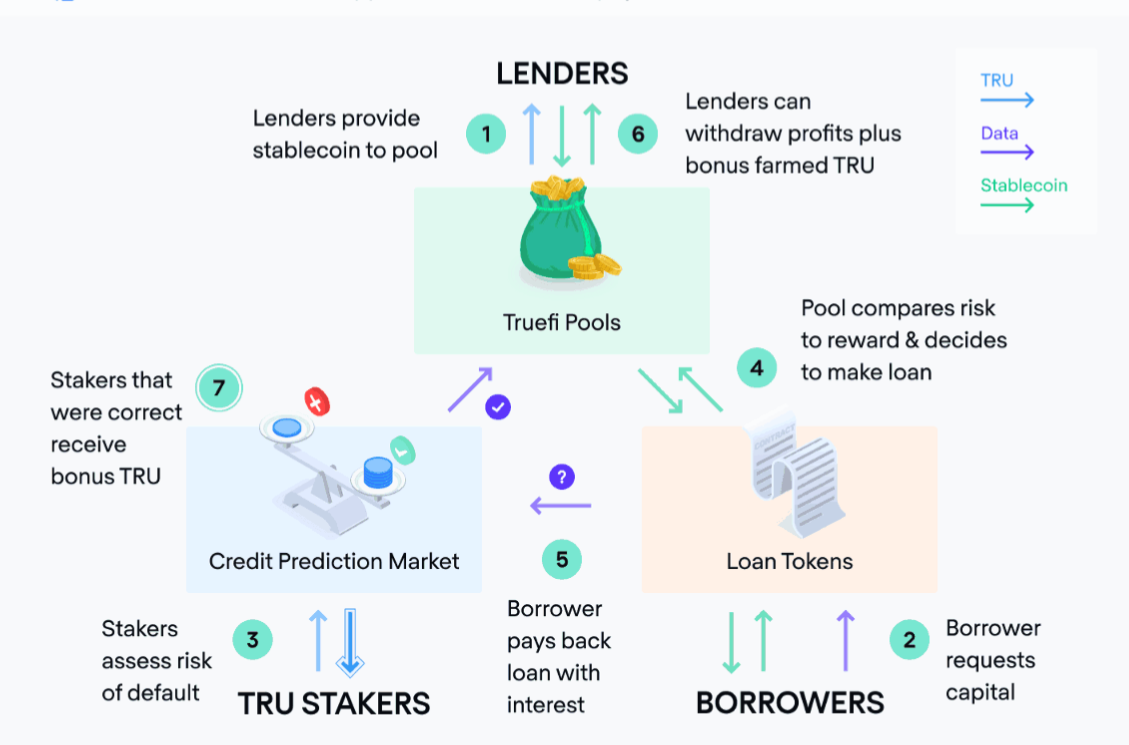

Lender (LP)

Liquidity providers, often referred to as LPs, play a pivotal role by contributing stablecoins like TUSD to the TrueFi lending pools. Borrowers in these pools pay interest, ensuring LPs earn returns in the original asset. However, when assets remain unutilized due to a lack of borrowers, they are seamlessly routed via the CURVE protocol (CRV), maximizing profitability.

TrueFi’s approach to idle assets sets it apart from other DeFi protocols. Assets in the lending pool are deposited into the CURVE protocol, allowing LPs to enjoy higher returns. This unique mechanism ensures that assets are moved into the lending pool only when TrueFi can offer a higher interest rate than existing DeFi stablecoin yields, such as those provided by Curve.

Liquidity providers receive tradeable ERC-20 tokens known as LP tokens, bearing the “tf” prefix, in exchange for depositing assets into lending pools. These tokens represent an LP’s proportional ownership in a lending pool and maintain a 1:1 peg to the underlying asset until the lending pool processes loans. As loans are repaid with interest, the lending pool’s net present value grows, boosting the value of LP tokens. Subsequent LPs entering the pool receive tokens at their current, increased value.

The journey doesn’t stop here. LPs can opt to deposit their LP tokens in the Liquidity Gauge farm, where they earn TRU tokens. These TRU rewards are distributed across lending pools, governed by the TrueFi community. This innovative incentive system encourages LPs to keep their deposits intact while contributing to the broader TrueFi ecosystem. Moreover, LPs have the option to stake their TRU rewards from the farm into the TRU staking pool, further amplifying their TRU returns.

In summary, LPs stand to benefit from three distinct sources of yield when providing liquidity to TrueFi lending pools:

Notably, rewards are distributed hourly and can be conveniently tracked in the TrueFi treasury. However, it’s essential to understand that in the current version of TrueFi, participants must manually claim and re-stake their rewards for compound interest.

This process involves two separate transactions on the Ethereum blockchain. LPs are advised to adjust the frequency of reward-claiming and re-staking based on the Annual Percentage Yield (APY) to optimize their returns, as gas fees may offset short-term gains from smaller stakes until automation is implemented.

Borrower

TrueFi has implemented a stringent Know Your Customer (KYC) and Anti-Money Laundering (AML) process, ensuring that only institutional entities are eligible for borrowing. These borrowers must also enter into legally binding contracts with TrustToken. Notably, all loan-related disputes are resolved through the binding arbitration laws of California. Moreover, borrowers located in jurisdictions where contract enforcement is impossible are automatically disqualified from onboarding.

One of the standout features of TrueFi is the way in which loan approvals are handled. Instead of relying on a traditional lender or intermediaries, TrueFi empowers TRU Stakers with the authority to approve or decline loans. When borrowers submit their loan requests, TRU Stakers cast their votes, either in favor (“Yes”) or against (“No”). This process underscores the importance of community governance in the TrueFi ecosystem.

The decision-making process doesn’t stop at a simple “Yes” or “No.” TRU Stakers who vote correctly, based on whether the borrower can repay the principal and interest before the due date, are rewarded with a share of TRU tokens from those who voted incorrectly. This mechanism incentivizes accurate decision-making and ensures the platform’s integrity.

TrueFi prioritizes transparency in its onboarding process. Once the legal contracts are sealed, detailed borrower information is publicly posted in the TrueFi governance forums. This information includes the organization’s background, historical performance, legal and financial status, and borrowing objectives. Every new borrower request is subject to on-chain community voting by TRU Stakers. If approved, borrowers can proceed to request loans after providing a whitelisted wallet address.

In the fast-evolving world of DeFi, Maple Finance has emerged as a pioneering platform, opening the doors for everyday users to participate in the corporate credit market built on the Ethereum and Solana blockchains. This innovative project allows users to lend tokens hosted on these two blockchains to institutions, promising profitable returns through interest repayments.

Maple Finance’s core proposition lies in its accessibility. Unlike traditional lending platforms, which may require substantial capital, Maple Finance welcomes users with as little capital as they have. This democratizes lending, making it an attractive option for a broader spectrum of cryptocurrency enthusiasts. Maple Finance is also one of the potential uncollateralized lending projects that attracts users.

Staking: Earning While You Hold MPL Tokens

Maple Finance’s staking feature empowers users to earn interest on their MPL tokens by actively supporting the platform’s operations. Stakers contribute their tokens to verify transactions on the blockchain, receiving a portion of the fees collected as a reward.

What sets Maple Finance apart is its monthly distribution of MPL tokens to all xMPL holders, ensuring a continuous flow of interest for token holders. Additionally, xMPL tokens grant users voting privileges to influence key decisions within the Maple ecosystem, such as buybacks and revenue allocation.

Lending: Diversified Opportunities for Earning Interest

The lending feature of Maple Finance provides users with access to various lending pools where they can deposit their assets and earn interest. The platform primarily operates with tokens from the Ethereum and Solana blockchains, predominantly USDC and wETH. To participate, users must have the respective tokens in their wallets.

Choosing a lending pool is a matter of personal preference, as users can deposit the relevant token from their wallet to initiate interest accrual. Prior to this, potential investors can access detailed performance reports for each pool, aiding in their decision-making process. While different pools offer varying interest rates, it’s essential to note that the final rate may fluctuate due to market conditions.

Borrowing: Accessing Capital with Flexible Terms

Maple Finance extends the opportunity for crypto investors to borrow funds from lending pools on its platform, with the flexibility to repay with interest. Borrowers utilize the tokens deposited by lenders in the pool for their investments, aiming to generate profits sufficient to cover interest payments and leave room for additional gains. The minimum loan amount available on Maple is $1,000,000.

To initiate the borrowing process, users are required to furnish identifying information, including their name, Twitter handle, Telegram handle, and email address. Subsequently, the selected lending pool’s delegate will review the application, conducting due diligence that includes know-your-customer and anti-money laundering checks.

Once the request is approved, borrowers can negotiate the loan’s terms and receive the funds in their Maple-connected wallet. Interest payments become due through the Maple web platform, providing borrowers with a user-friendly and efficient experience.

In the fast-evolving world of decentralized finance (DeFi), most platforms mandate over-collateralization for loans, a practice designed to safeguard against defaults. However, a pioneering DeFi platform called Goldfinch Finance is disrupting this norm, offering borrowers the opportunity to secure loans without the burden of providing cryptocurrencies as collateral.

Goldfinch Finance, which operates on the Ethereum blockchain, was established in July 2020 by co-founders Mike Sall and Blake West, both former employees of Coinbase. The platform’s primary mission is to democratize access to affordable and accessible lending options for businesses globally, marking a significant departure from traditional DeFi practices.

While most DeFi platforms require users to over-collateralize their loans, Goldfinch Finance is introducing a paradigm shift by enabling borrowers to access capital without the need for cryptocurrency collateral. This innovative approach paves the way for a more inclusive and efficient lending ecosystem, further bridging the gap between the crypto and traditional financial worlds.

A Credit Scoring Revolution

Goldfinch’s “trust through consensus” credit scoring system evaluates borrowers’ creditworthiness based on their past behavior, providing a more holistic view for lenders. By enabling complete collateralization with off-chain assets and income, the platform offers increased security and flexibility, making it a standout choice for borrowers.

Business-Oriented DeFi Lending

One of Goldfinch’s key differentiators is its focus on business clientele, making it one of the first DeFi lending protocols tailored to this niche. This opens up new avenues for entrepreneurs and SMEs seeking decentralized financial solutions.

Leveraging Off-Chain Yield Sources

The Goldfinch protocol effectively harnesses off-chain sources of yield and integrates composable DeFi elements to enhance Return on Investments (ROIs) for lenders.

Customizable Loan Terms

Borrowers have the freedom to propose loan terms, including interest rates and repayment schedules. Backers can evaluate these options and decide whether to fund the junior tranches of Borrower Pools, giving borrowers more control over their borrowing experience.

Attractive Returns

The network offers an average of 10-14% Annual Percentage Yield (APY) on lending and staking activities. These returns are automatically deposited into your network wallet, providing a low-risk, passive income stream with asset security.

Senior Pool Participation

By supplying capital to the Senior Pool, users actively support the system, and their contributions are automatically allocated to the senior tranches of Borrower Pools. Real-time tracking via a blockchain explorer ensures transparency.

Senior Pool Liquidity Mining

Goldfinch’s liquidity mining protocol offers 8.0% of tokens as returns, incentivizing long-term Liquidity Providers and boosting adoption. The 12-month lock period ensures asset security, and rewards can be reinvested to enhance future staking rounds.

Stake for Consensus and Security

Staking GFI tokens with specific Backers not only improves consensus times but also adds an extra layer of protection against default loans in borrower pools. This safeguards lenders’ investments and maintains the protocol’s financial health.

Clearpool Finance, a prominent unsecured lending platform operating on both Ethereum and Polygon, has successfully secured $3 million in funding from various well-known investment firms. This infusion of capital is poised to accelerate Clearpool’s mission of facilitating borrowing and lending in the crypto space. Clearpool is one of the uncollateralized lending projects with huge backers.

The funding has been sourced from a consortium of reputable funds, including Arrington Capital, HashKey, Sequoia India, Sino Capital, Wintermute, FBG Capital, Huobi Ventures, and Kenetic Capital. With this substantial backing, Clearpool is well-positioned to enhance its services and expand its reach in the decentralized finance (DeFi) sector.

Clearpool’s platform closely resembles TrueFi, as it caters to two distinct user groups: Borrowers and Lenders. Borrowers are typically companies seeking to secure loans within the crypto ecosystem, while Lenders are crypto enthusiasts or investors willing to provide loan capital.

Clearpool Finance operates with two primary types of lending pools: Permissionless and Prime. In both cases, Borrowers are required to submit loan applications for approval by Clearpool before funds are granted. However, the two pools differ in their approach to Know Your Customer (KYC) requirements.

LayerZero Integration for Seamless CPOOL Token Transfers

With the recent integration of LayerZero technology, Clearpool Finance has taken a significant step towards improving user experience. This integration enables the seamless transfer of CPOOL tokens across multiple blockchain networks. It enhances Clearpool’s accessibility and streamlines the lending process for users.

Diverse Clientele with a Unique Twist

Clearpool Finance proudly counts several prominent customers among its clientele, including Amber Group, Nibbio, Wintermute, Folkvang, FBG Capital, Bastion Trading, Auros, and Portofino Technologies. These clients share similarities with TrueFi but choose Clearpool for their lending needs, albeit on a smaller scale.

Impressive Returns on Stablecoins

A standout feature of Clearpool Finance is its ability to generate an average return of 12% on Stablecoins. This includes CPOOL rewards for lenders, which significantly outperform traditional collateral lending protocols like Aave, typically offering returns in the range of 2-3%.

Future Expansion and Product Offerings

Clearpool Finance has ambitious plans for the future. The platform intends to expand its lending services to encompass a wider array of assets. Additionally, Clearpool will introduce new products, such as Exchange Traded Pools and Secondary Trading, aimed at serving an even broader range of customers within the DeFi ecosystem.

cpToken – A Game Changer

A key innovation introduced by Clearpool is the concept of cpTokens. These tokens represent the amount of liquidity provided to a pool, accrue interest per block, and reflect the risk profile of the borrower. Notably, cpTokens are redeemable based on available liquidity and can be traded on the secondary market, providing liquidity providers (LPs) with an additional source of liquidity and risk management.

Moreover, cpToken holders will receive added incentives in the form of CPOOL rewards, positioning Clearpool as one of the most attractive lending platforms in DeFi.

Thematic Pools

Thematic Pools are multi-borrower liquidity pools administered to conveniently provide Clearpool liquidity providers with the benefits of diversification. The liquidity distributed to these pools is algorithmically managed, providing a rebalanced approach based on the pool governance’s approved mandate.

Launched in early 2020, Atlendis has been making waves in the DeFi world due to its innovative development orientation, which currently centers on Ethereum and Polygon, albeit with a primary deployment on the Polygon network. Atlendis is one of the uncollateralized lending projects that offers many options for users.

Atlendis, at its core, is a DeFi credit protocol designed to offer lending services to real-world businesses. Unlike traditional lending institutions, this platform operates on the Ethereum blockchain, leveraging a combination of on-chain and off-chain data to meticulously assess the creditworthiness of potential borrowers. This multifaceted approach ensures that Atlendis maintains a robust and reliable credit evaluation system.

PSAN Certification: Paving the Way for Regulatory Compliance

Atlendis has recently obtained the PSAN (Prestataire de Services d’Actifs Numériques) license, which is tantamount to a license for cryptocurrency service providers in France. This achievement underscores Atlendis’ unwavering commitment to adhering to the stringent cryptocurrency regulations in France. Moreover, this certification serves as a precursor for Atlendis to align seamlessly with the upcoming MiCA (Markets in Crypto-Assets) regulations in Europe.

The PSAN license, effectively a seal of approval, also presents a template for the compliance requirements that lie ahead, positioning Atlendis at the forefront of regulatory compliance in the ever-evolving crypto landscape.

Empowering Innovation with BPI’s 1 Million Euro Loan

Atlendis’s second milestone is equally momentous, as they have successfully secured a loan of 1 million euros from BPI (Banque Publique d’Investissement), the French national investment bank. This financial injection is set to fuel the development and launch of ‘Atlendis Flow,’ a pioneering product designed to streamline decentralized lending operations for borrowing organizations. Atlendis Flow is poised to revolutionize the lending landscape by providing efficient and innovative solutions to businesses seeking decentralized lending options.

Strategic Partnerships in the Alternative Finance Sector

In addition to these achievements, Atlendis has cemented strategic partnerships with several fintech companies operating in the Alternative Finance sector. These collaborations will empower Atlendis to offer a diverse range of financial services, including:

DISCLAIMER: The information on this website is provided as general market commentary and does not constitute investment advice. We encourage you to do your own research before investing.

Discover why Qubetics, NEAR Protocol, and Immutable X are the best altcoins to join today,…

BTFD Coin is offering a chance to relive the glory days of meme coin investing,…

Explore key takeaways from BlockDAG’s AMA, showcasing strides in scalability, growth of the ecosystem, and…

Discover why Qubetics, Polkadot, and Cosmos are the best cryptos with 1000X potential, offering innovation,…

Explore the best coins to buy in December 2024—Qubetics with its thrilling presale, Polkadot’s interoperability,…

The Crypto Market Outlook 2025 highlights key areas: stablecoin growth, tokenization, crypto ETFs, DeFi innovation,…

This website uses cookies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}